Common mistakes founders make in financial models

Of course, things will never play out exactly as projected but it gives you guidance and trust on how to move forward.

First of all, a financial model should mainly support you in projecting your business and evaluating different scenarios. Yet, the financial model is also a key part of a due diligence. Hence, we would like to highlight the common mistakes we see when evaluating financial models.

Computing the financial projections is in most cases already relevant prior to generating any revenues as it show cases your knowledge about the business model, its unit economics and how you are planning on generating revenues. Of course, things will never play out exactly as projected but it gives you guidance and trust on how to move forward. The quality of the financial model has a big impact on the risk perception of the investor. Mistakes can lead to a bad position during the negotiations and these mistakes are not only connected to unrealistic revenue projections! For the first article of this series about common mistakes in financial models, we will focus on structure and design. So, let’s dive into it.

Annual view only

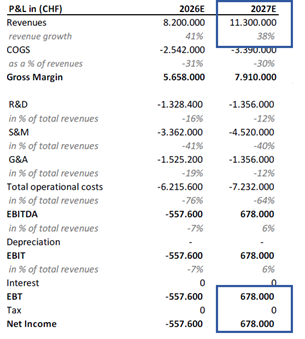

The easiest way to explain this mistake is by looking at an example. Below, there is a hypothetical P&L that shows the projections of 2026 and 2027. The marked areas are the revenues and the Earnings before Taxes (EBT).

The first impression is positive as the company generates revenues and is reaching its break-even by not making a loss anymore (in comparison to 2026).

However, in an extreme example it could be that the revenues of CHF 11,3m are generated only in the second half of the year. So, what would happen in the first half of the year? The answer is that only costs will incur and the company might not be able to cover them.

It is essential for a founder to understand the cashflow mechanics. These mechanics help you as a founder to understand how much funding you will need and when. This cannot be done on an annual basis only. This example shows two important points:

1. A cashflow statement is a must-have

2. A monthly perspective is a must-have for the cashflow statement and highly recommended for the P&L

While the P&L could also be only displayed annually, it would take away the founders’ chances to present their knowledge about seasonality within the industry. Financial projections are hard enough, so you should take every chance to convince investors that you know your market and the business model in every detail.

Hard coded revenues

Hard coded numbers can create intransparency and frustration when an investor tries to understand how certain values (especially revenues) are derived.

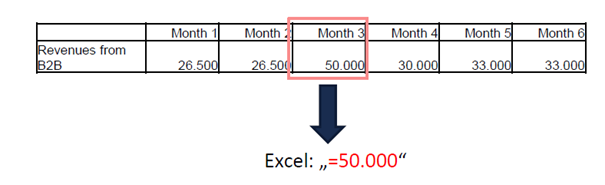

Let’s assume an investor sees the revenue line in the table below (Excel format):

The investor will be interested in the revenue development over time. Revenues spike in the 3rd month which can be reasonable, but why is that? Is it because there is an increase in new clients or because existing clients have increased their order volume? It is not clear by just looking at the number the way we see it now. The investor will try to understand where the 50k in revenues come from and it’s your job to guide them through the number. Clicking on a hard coded “50.000” with no further information can be frustrating and will most likely lead to a long list of questions during the financial Due Diligence (which delays the process even further).

We advise you on having a clear logic for each number in the P&L and that an investor can easily understand how a certain number was calculated.

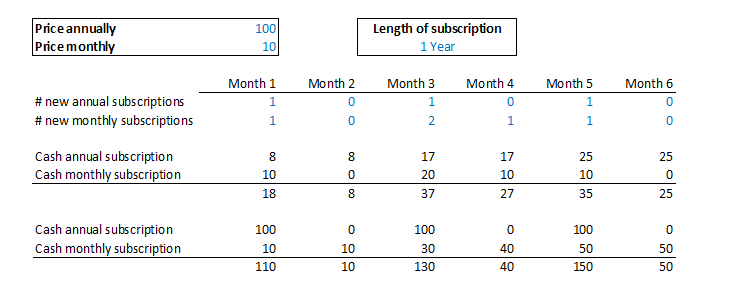

Color code

Having a clear color code is essential for every financial model regardless of the industry a startup is operating in. The pictures below show the same model, but one indicates assumptions (blue) and formulas (black) with a color code. It makes every analysis faster as an investor or even you as the founder doesn’t need to check if a figure is an assumption or a formula.

Without colour code:

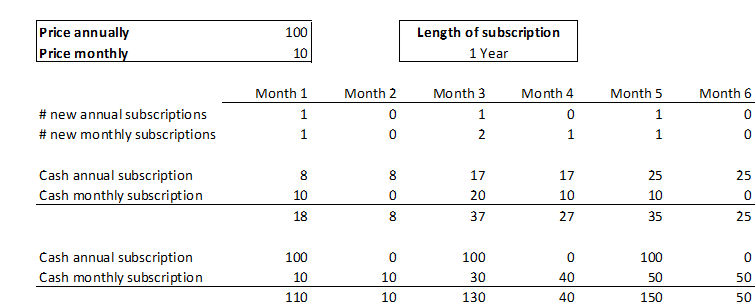

With colour code: